Tokenization Trends in 2025: How Real-World Asset Tokenization is Reshaping Global Finance

In 2025, real-world asset tokenization matured into a real part of the financial system. Treasury portfolios, credit funds and equity instruments moved onchain at scale, with Centrifuge positioned as a top platform driving this transformation in global finance.

Below are 5 trends and 25 numbers from 2025 that capture the scale of this shift.

Institutional Capital Commits at Scale

The clearest signal this year came from the types of products institutions chose to bring onchain.

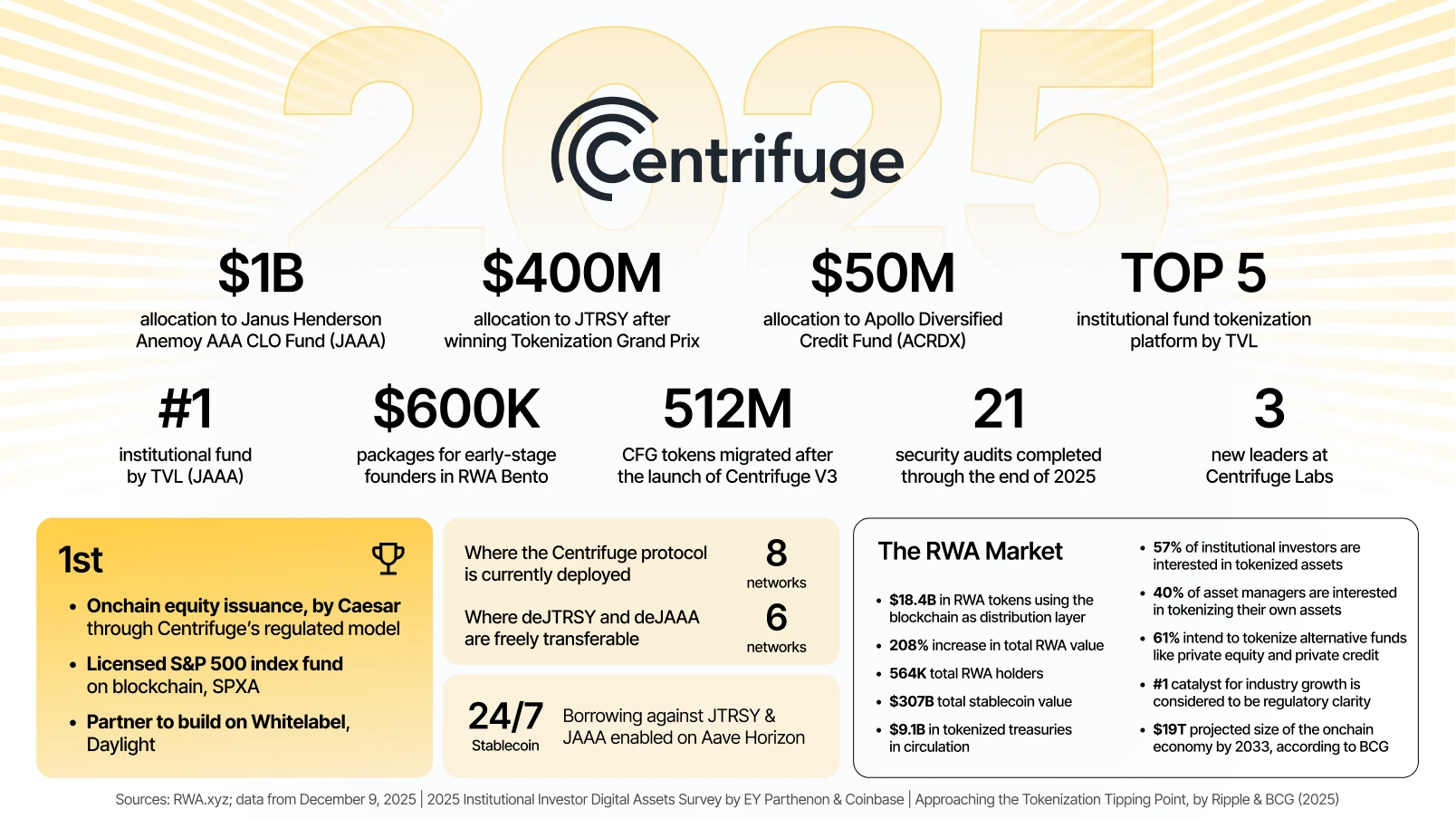

1. JTRSY received $400M in allocations: After winning Spark's Tokenization Grand Prix, the Janus Henderson Anemoy Treasury Fund received a $200M allocation that expanded to $400M. It's currently one of the largest tokenized treasury products onchain.

2. JAAA exceeded $1B in TVL: Janus Henderson then brought its AAA CLO strategy fully onchain, which received a significant allocation from Grove, the institutional credit platform incubated in the Sky ecosystem.

3. JAAA stands as the #1 institutional alternative fund onchain by asset value.

4. ACRDX launched with a $50M allocation: A fund that provides onchain access to Apollo Diversified Credit Fund, a diversified global credit strategy investing across corporate direct lending, asset-backed lending, performing credit, and dislocated credit.

5. Top 5 platform by TVL: Across these products, Centrifuge ranks among the five largest fund tokenization platforms by asset value.

Infrastructure Matures for Regulated Issuance

6. Centrifuge V3 was deployed across 8 networks: The new protocol introduced a unified, EVM-native architecture designed for institutional scale. By year-end, Centrifuge operates across Ethereum, Base, Arbitrum, Avalanche, Plume, Solana, Stellar and BNB Chain, with asset managers enabled to launch tokenized funds directly in the environments where their investors already operate and hold digital assets.

7. 512M CFG tokens migrated: As part of the V3 upgrade, the protocol consolidated CFG into a single ERC-20 on Ethereum. Roughly 91% of the token supply migrated to the new token, aligning the community with the new architecture.

8. Centrifuge completed 21 independent audits, 15 of them this year alone, covering core protocol components and the new multichain stack. All reports remain public for full transparency.

Tokenized Funds Become Composable DeFi Building Blocks

Composability turns tokenized funds from passive investments into infrastructure that protocols and institutions can build upon.

9. deRWA expanded across 6 networks: deJTRSY and deJAAA now exist as freely transferable tokens across Ethereum, Base, Arbitrum, Avalanche, Solana and Stellar. Institutional strategies have the same transferability as native DeFi assets.

10. JAAA and JTRSY became 24/7 collateral on Aave Horizon: Holders can unlock liquidity by borrowing stablecoins against treasury and credit positions, transforming them into working balance-sheet tools for trading, hedging and cash management.

11. $600K packages for builders: For early-stage teams, Centrifuge and Onigiri launched RWA Bento, offering selected founders $500K in capital and $100K in Centrifuge infrastructure credits, and targeting founders with distribution advantages.

Asset Classes Expand Beyond Treasuries and Institutional Funds

Tokenization stretched into new territory in 2025.

12. First crypto-native equity issuance: Caesar became the first crypto-native company moving toward equity issuance onchain through Centrifuge's SEC-registered transfer agent model for tokenized securities, with shares represented directly as digital tokens maintaining full shareholder rights and transparent asset ownership.

13. First licensed S&P 500 Index fund onchain: SPXA launched as the first licensed S&P 500 index fund on blockchain, running on Base with Centrifuge's Proof-of-Index infrastructure and offering direct equity exposure within onchain portfolios.

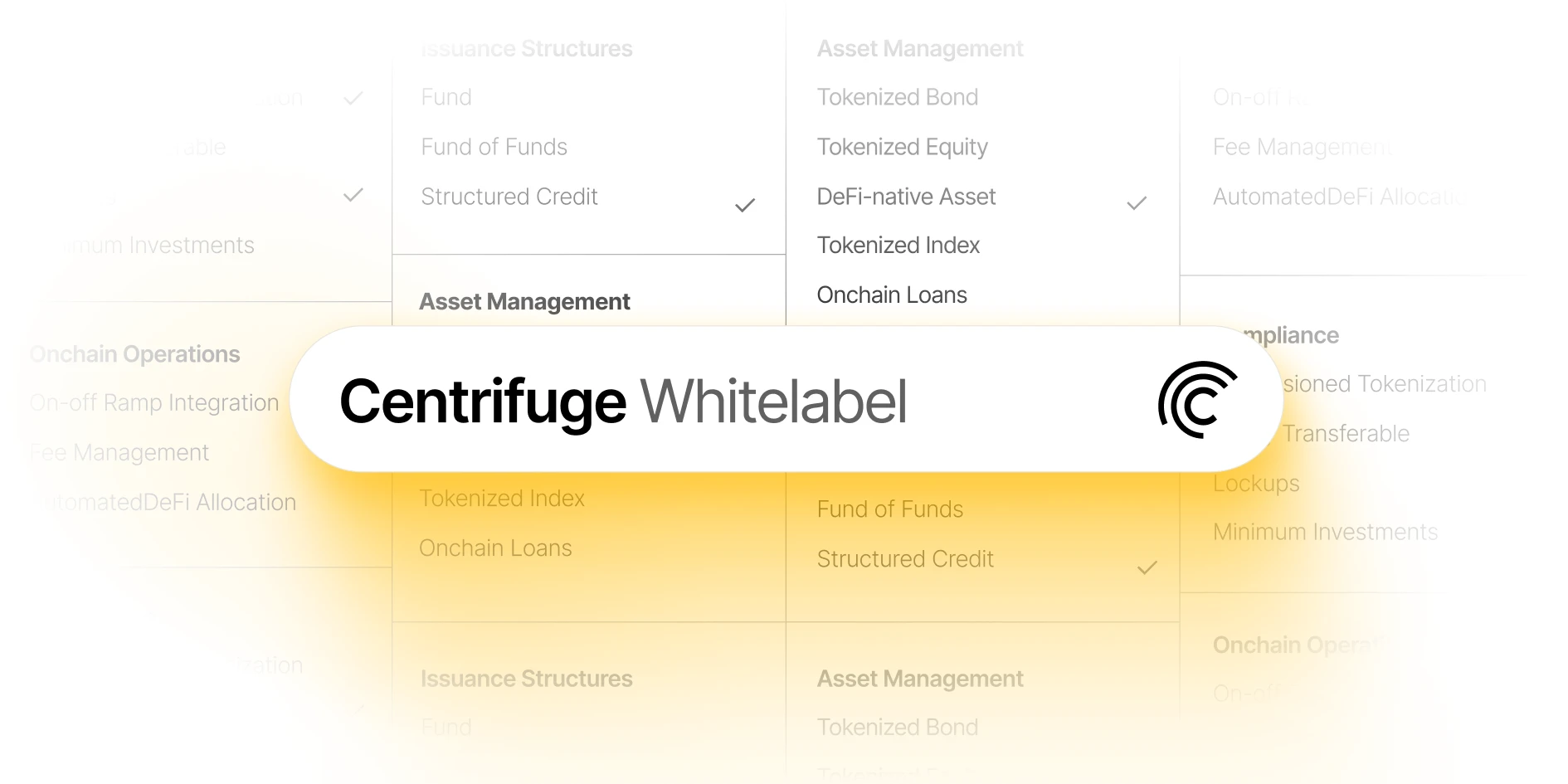

14. First team to build with Centrifuge Whitelabel: Daylight became the first external team to use Centrifuge’s whitelabel offering. They tokenize electricity revenues from solar and storage assets with NAV calculations, redemptions and cross-chain liquidity for the underlying assets handled by an audited infrastructure of smart contracts.

The Broader Market Reaches Escape Velocity

15. Tokenized RWAs reached $18.4B: Relative to traditional finance it is still early, but compared to where RWAs stood a few years ago, it marks the start of a different category.

16. RWA value grew 208% YTD: The onchain RWA market expanded rapidly, driven first by treasury products and then by credit strategies and institutional funds.

17. RWA holders currently at 564K: Up from 84,000 at the start of the year, as participation from institutions and retail investors continues to scale.

18. Stablecoin market at $307B: The market rose from $204B at the beginning of the year. Capital is going onchain independent of crypto volatility, and supporting settlement flows across tokenized funds.

19. Tokenized treasuries at $9.1B: They account for nearly half of all onchain RWA value, and kept their position as the segment’s early proof point for global liquidity into real world assets onchain.

What Comes Next: Institutional Roadmap

Survey data from Coinbase and EY Parthenon shows where this heads.

20. 57% of institutional investors expect to allocate to tokenized assets, motivated by faster settlement, better yield access and standardized entry into private markets.

21. 40% of asset managers intend to tokenize their own products, citing faster settlement, improved liquidity and fractional ownership benefits.

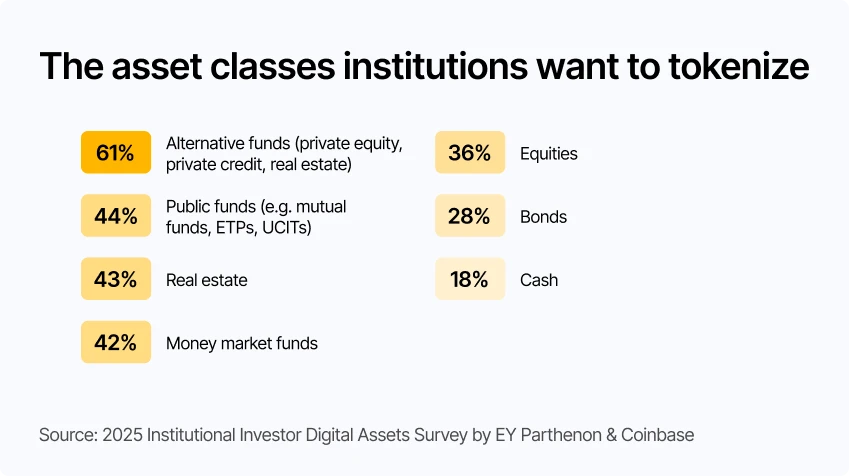

22. Asked which products they would tokenize first, asset managers cited alternative funds like private equity and private credit (61%), then public funds (44%), real estate (43%), money-market funds (42%) and equities (36%).

23. Regulatory clarity remains the top catalyst: When asked what would accelerate adoption fastest, their top request was clear legal frameworks around tokenized structures, followed by broader institutional adoption and retail familiarity.

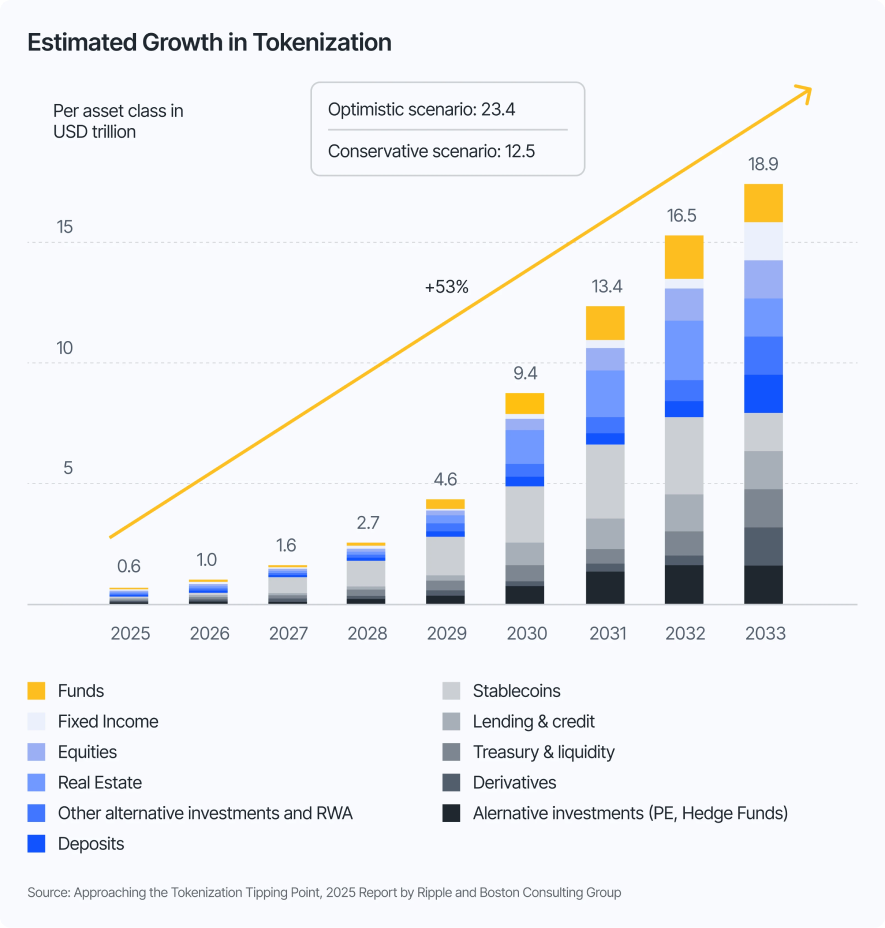

24. $19T projection by 2033: Boston Consulting Group and Ripple estimate that tokenization could reach $19 trillion by 2033, close to a tenth of global GDP.

Carrying 2025’s Momentum Into 2026

25. A new leadership team led a defining year: Bhaji Illuminati stepped into the CEO role, Anil Sood took on the role of Chief Strategy and Growth Officer, and Jürgen Blumberg joined as COO.Together with the broader team, they shaped Centrifuge’s 2025 trajectory and are now pushing the work forward into 2026.

Scaling RWAs from billions to trillions requires infrastructure institutions can activate immediately: tooling that enables regulated products to launch without rebuilding everything from scratch. Centrifuge delivers that foundation through audited components, regulated frameworks and modular systems that turn tokenization from a technical challenge into a deployment decision.

The institutions moving fastest are choosing infrastructure that’s already proven at scale. And in 2026, tokenization moves from early adoption to full deployment.

.webp)

Ready to get started?

Centrifuge’s real-world asset tokenization platform brings the full power of onchain finance to asset managers and investors.