Centrifuge Tokenized Equities: A Reference Architecture for Regulated Onchain Equity

Centrifuge has introduced a regulated model for tokenized securities that allows real corporate equity to exist directly on public blockchains while remaining anchored in U.S. securities law through an SEC-registered transfer agent. This structure enables companies to issue and manage tokenized equities that can be held either in traditional book-entry format, like any traditional stock, or as onchain tokens on blockchain-based platforms, with each form recorded in a unified, legally authoritative shareholder ledger.

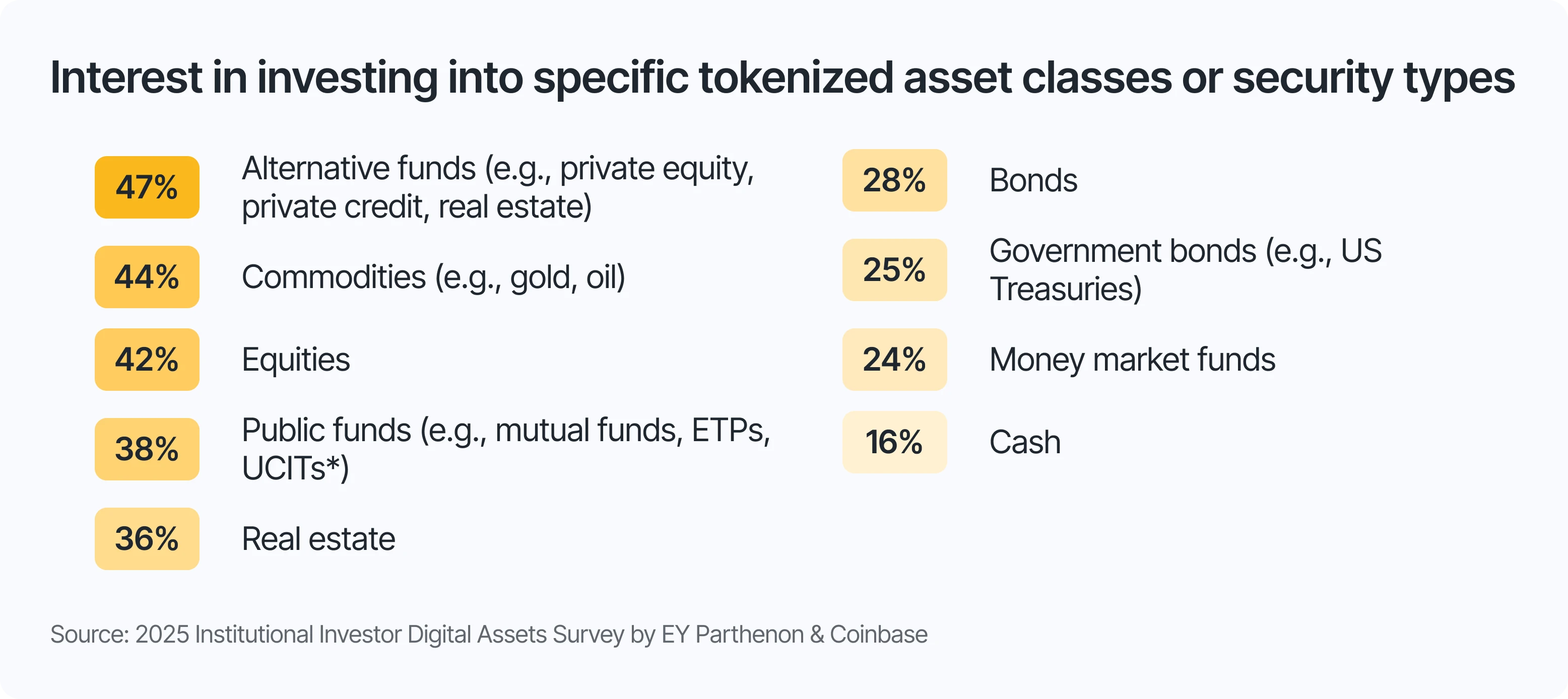

Investor interest in tokenized assets is accelerating. According to a 2025 survey by Coinbase and EY-Parthenon, 42% of institutional investors are interested in tokenizing equities, alongside 47% for alternative funds and 44% for commodities. Notably, 72% of respondents plan to begin investing in tokenized assets by 2026. This surge in intent underscores why a legally robust infrastructure, like the one Centrifuge offers, is needed now more than ever.

The tokenized shares Centrifuge creates are not wrappers, derivatives, or SPV claims. They are the underlying shares themselves, represented as digital tokens on a blockchain and reconciled continuously by Centrifuge’s transfer-agent infrastructure. In doing so, Centrifuge is creating the foundation for a modern capital-markets architecture where corporate ownership can be transparent, programmable, and globally transferable, giving investors direct exposure to real-world equities without stepping outside the existing regulatory perimeter.

This paper outlines the architecture Centrifuge is bringing to market, the regulatory and technological foundations beneath it, and the implications for issuers, investors, asset managers, and tokenized economies seeking an operationally robust ownership framework for tokenized assets, from private companies to eventually publicly traded equities, built on blockchain technology and aligned with securities regulation.

Onchain Equities at the Intersection of Innovation and Traditional Markets

Capital markets have always evolved at the edge of innovation and regulation, and the rise of digital assets has brought this tension into sharper focus. Crypto-native companies, in particular, operate in an environment where decentralized networks, smart-contract–based systems, and global accessibility offer advantages that traditional markets cannot match, such as near-instant settlement, transparent ownership, and the ability to move capital 24/7. At the same time, traditional equity remains the legally recognized foundation for corporate formation, investor protections, voting rights, governance structures, and institutional participation across global markets.

Centrifuge’s architecture for tokenized assets is designed precisely to bridge these two worlds. By leveraging its role as an SEC-registered transfer agent, Centrifuge enables issuers to express their equity directly on public blockchains while still operating inside established securities frameworks. The blockchain becomes a shared digital ledger, an infrastructure layer for recordkeeping and settlement, without replacing the legal rights, shareholder protections, or regulatory expectations that define ownership of traditional stocks and other financial instruments today.

This model is arriving at a time when tokenized equities and various real-world assets are rapidly gaining traction. Analysts estimate that global tokenized markets could reach into the trillions as traditional finance integrates with blockchain-based platforms.

A BCG forecast projects that the market for tokenized assets could grow from $0.6 trillion today to $18.9 trillion by 2033 — or as much as $23.4 trillion in an optimistic scenario. While this includes everything from stablecoins to credit markets, tokenized equities, real estate, and funds represent major drivers of this transformation.

Even today, tokenized stocks on centralized and decentralized platforms allow investors to gain exposure to real-world equities, though most of these products do not confer voting rights or formal shareholder status. The core innovation of Centrifuge’s model is that the tokens represent the actual underlying shares, not derivatives or exposure-only products, a distinction that unlocks regulated, investor-ready onchain ownership.

Caesar AI will be among the first issuers to use this architecture. As a crypto-native organization with contributors, investors, and early stakeholders accustomed to onchain participation, Caesar represents a new category of companies ready to evolve beyond utility tokens and into real, regulated corporate ownership. Their adoption of tokenized equity demonstrates why this model is becoming a natural next step for high-growth crypto projects seeking to institutionalize while preserving the transparency, programmability, and global reach that define onchain systems.

Crypto-Native Cap Tables and Tokenized Stocks: A Different Starting Point

Most companies exploring tokenized equities approach the transition from the perspective of traditional securities infrastructure: centralized cap tables, custodians, brokers, transfer restrictions, and investor records that flow through regulated intermediaries. Crypto-native organizations begin almost at the opposite extreme. Their ownership structures are shaped by tokens, decentralized wallets, community-driven governance, and global participation that looks nothing like the ownership frameworks of traditional stocks.

For years, this model enabled rapid experimentation and global distribution. Contributors earned value through onchain work, delegation, bounties, or protocol-level incentives. Stakeholders were recognized by their public keys, not their brokerage accounts. Liquidity expectations were conditioned by the fluid, 24/7 nature of digital assets, far removed from the opening hours of a traditional stock exchange. Transparency, fractional ownership, and programmability were inherent features, not add-ons.

But as crypto-native companies scale, they encounter structural needs that utility tokens or governance tokens cannot satisfy: enforceable ownership rights, standardized governance, long-term incentive structures for employees, and the ability to raise capital from regulated investors who cannot hold unregistered crypto assets. Hybrid systems, where tokens coexist with offchain equity records, partially solve these challenges, but they often create fragmented ledgers, duplicate incentive systems, and misaligned economic exposure between token holders and shareholders.

This is the moment when a regulated onchain equity model becomes essential. Centrifuge’s architecture enables a crypto-native company to evolve without abandoning its onchain DNA. Instead of moving contributors into legacy corporate systems or relying on offshore structures, companies can merge decentralized participation with a regulated cap-table framework expressed through tokenized shares. Equity becomes as transparent and composable as other onchain assets, while retaining the durability, investor protections, and governance rights that define real-world equities in traditional finance.

Case Study: Caesar AI transitions to onchain equity

- Issuer: Caesar AI, a crypto-native AI co-research platform.

- Transfer Agent: Centrifuge, serving as the SEC-registered transfer agent and onchain cap-table provider.

- Asset Type: Direct tokenized equity representing the underlying shares themselves, not a derivative instrument.

- Shareholder Rights: Token holders receive the same governance, information, and economic rights as holders of traditional stocks.

- Access Controls: Only investors who complete KYC/AML with Centrifuge and are allowlisted can hold or transfer the tokenized shares.

These tokenized shares can be held in traditional book-entry form or as onchain tokens recorded on a public blockchain, both formats tied to a single, authoritative shareholder ledger maintained by Centrifuge.

The Evolution of Equities: From Traditional Stocks to Onchain Shares

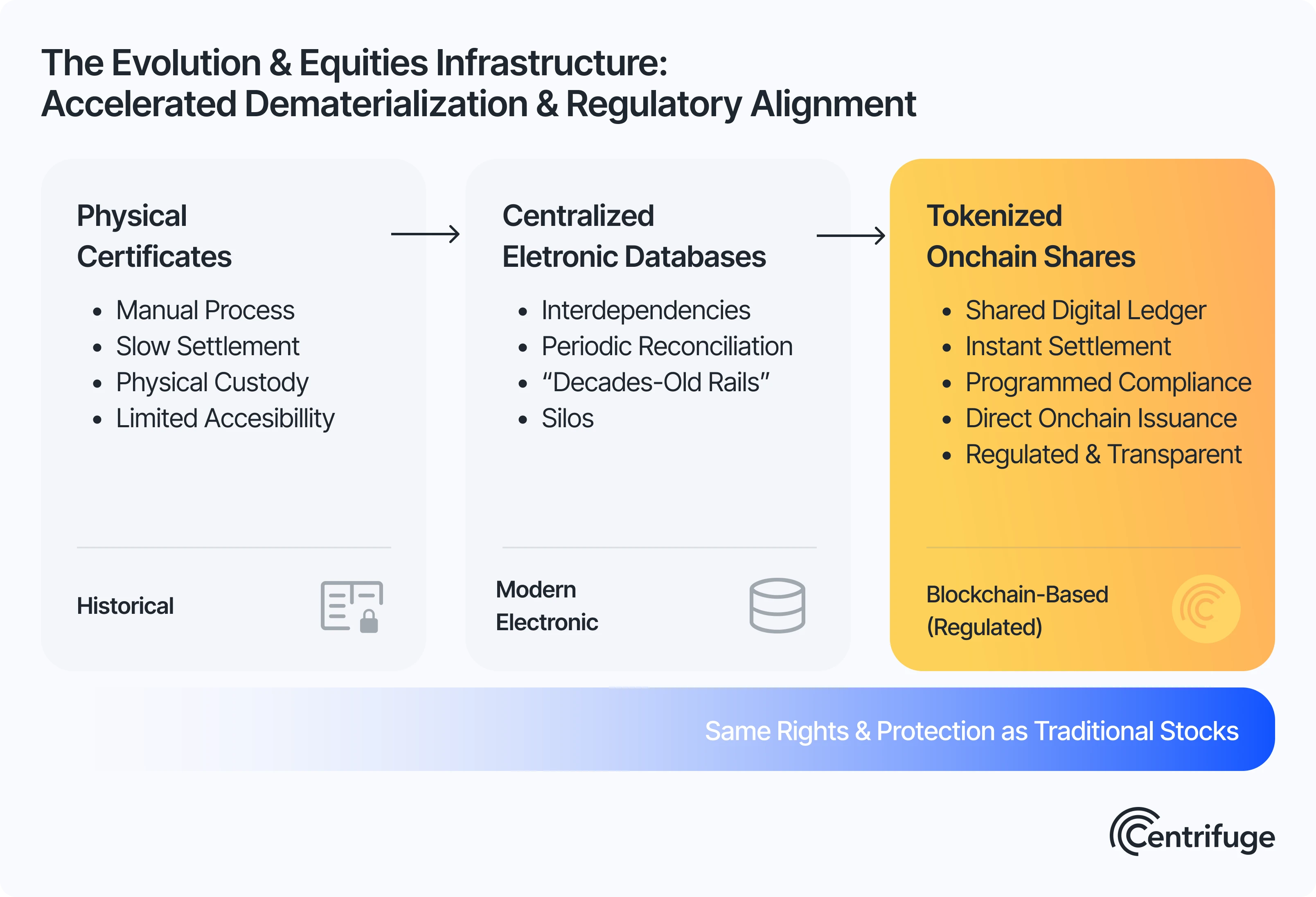

The evolution of equities, and the broader securities industry, has always mirrored advances in infrastructure. What began as paper certificates gradually transitioned into centralized databases like DTCC, bringing scale while adding layers of intermediaries, custodians, and reconciliation cycles. Today, most traditional stocks and listed equities exist only as electronic entries inside proprietary systems. Even though investors rarely interact with physical certificates anymore, the market still relies on decades-old rails to manage ownership, settlement, and corporate actions.

Tokenization accelerates the next phase of this dematerialization. It is not a reinvention of the underlying shares or the economic exposure they provide, it is a redesign of how ownership is recorded, transferred, and enforced. Rather than relying on siloed databases, blockchain technology introduces a shared digital ledger where settlement finality, transparency, ordering, and auditability are intrinsic features, not services outsourced to intermediaries. This is why tokenized stocks, and other tokenized assets are increasingly seen as the natural extension of an already-digital market.

For more than a decade, the industry has demonstrated that tokenization is technically feasible. Stablecoins, tokenized money market funds, and onchain credit products already show how financial instruments behave when moved to blockchain-based platforms. These products track underlying assets, support fractional shares, and offer fast settlement across global markets. Yet despite their advantages, widespread adoption for real-world equities has been limited, not by technology, but by regulatory alignment.

Existing securities frameworks were designed for custodial systems, centralized exchanges, and broker-dealer workflows. They assume ownership is maintained by regulated custodians and updated through periodic reconciliation. They were not built for instant settlement, decentralized platforms, or investor-controlled wallets. As a result, even though equity tokens can mirror the price movements of traditional securities, stock tokens have struggled to enter the regulatory perimeter that governs public and private companies raising capital.

That environment is now shifting. Regulators are increasingly engaging with the industry to understand how blockchain-based settlement, programmable compliance, and transparent digital ownership can coexist with long-standing principles of investor protection and market integrity. Across the regulatory landscape, agencies are evaluating how tokenized securities should be classified, how corporate actions should be processed onchain, and how real-world equities can migrate to public blockchains without introducing new systemic risks.

Centrifuge’s model represents a practical, regulated step toward this future. By enabling companies to issue equity directly onchain through an SEC-registered transfer agent, it places tokenized equity firmly within the existing legal framework, something few companies have achieved. Instead of treating blockchain as an experimental add-on, this architecture uses it as the primary system of record while ensuring compliance with securities laws that have governed traditional finance for decades.

Bridging the Perception Gap: Tokenized Equity and the Full Capital Stack

Despite the progress of digital assets, a structural perception gap persists in how investors view traditional stocks versus tokenized equities. Institutional allocators: venture funds, pension vehicles, hedge funds, and strategic investors, often cannot hold utility tokens or other digital tokens due to custody requirements, risk constraints, and the broader regulatory landscape governing traditional securities. Even when tokens provide meaningful economic exposure, they rarely fit into the operational frameworks that the securities industry relies on: audited governance, regulated custody, and clearly enforceable ownership rights.

For crypto-native founders, this divide can feel counterintuitive. Tokens offer programmability, fast settlement, and global distribution across decentralized platforms. They enable contributors to earn value directly through onchain participation and allow communities to coordinate in ways traditional exchanges or brokerage accounts cannot. Tokens also created early precedents for fractional ownership, shared governance, and new forms of incentive alignment. Yet institutions still evaluate long-term investments through corporate law, shareholder protections, and the rigor of regulated financial instruments.

Tokenized equity, not just stock tokens, but actual equity recorded on a blockchain, closes this gap.

By representing underlying shares of a company directly on a digital ledger, companies can offer an ownership instrument that preserves the strengths of blockchain technology while meeting the requirements of traditional finance. Tokenized equity lets a crypto-native issuer present a single, unified capital stack accessible to every investor category: early token holders, contributors, angels, VCs, hedge funds, and long-only institutional capital.

The implications are profound. Founder teams no longer have to choose between a token-first strategy that may exclude large allocators, or a purely offchain structure that conflicts with their onchain identity. Regulated, onchain equity becomes the bridge: traditional equity, with the same rights, voting rights, and economic exposure as conventional stockholders, expressed through programmable smart contracts. This unlocks new investment opportunities, expands access to global markets, and brings public-company-grade ownership workflows into crypto-native ecosystems.

For investors, tokenized equity provides an instrument they already understand but with the advantages of blockchain-based platforms: transparent settlement, reduced intermediaries, and the potential for future integrations with DeFi tooling. Funds restricted from holding tokens can finally gain exposure to crypto-native companies by owning real-world equities, not synthetic instruments or wrapped products, recorded through a regulated model. Early contributors can convert participation into formal ownership, gaining the same shareholder status as institutional investors.

For founders, the capital pool widens dramatically. Traditional investors can participate through a structure aligned with their mandates, while crypto communities continue to operate onchain. This dissolves the long-standing boundary between “crypto capital” and “traditional capital” and creates a path for companies to raise, scale, and professionalize with the same tools used by the world’s most successful public companies.

This marks the beginning of a new architecture for tokenized assets, one in which crypto-native companies do not have to choose between legitimacy and innovation. They can maintain their onchain DNA while accessing the full spectrum of venture capital, institutional liquidity, and participation across global markets.

What Equity Tokenization Really Means

In this structure, equity tokenization is not a wrapper, not a synthetic exposure, and not a blockchain-based “stock token” that merely tracks stock price movements. It is not a claim on an offshore vehicle or a derivative tied to underlying stocks. Instead, tokenization refers to moving the official record of who owns the company’s underlying shares onto a public blockchain, under the supervision of a regulated, SEC-registered transfer agent. The result is a form of tokenized securities where the blockchain becomes the authoritative digital ledger for actual ownership, not a parallel representation.

At any point in time, outstanding equity can exist in one of two legally equivalent formats:

- Traditional book-entry form, recorded in the transfer agent’s systems and reflected in the issuer’s corporate records, similar to how traditional stocks are held today through regulated custodians and traditional exchanges; or

- Tokenized form, where the same shares are represented as tokenized shares at a specific address on a public blockchain, but still reconciled against the same official shareholder ledger.

In both cases, the holder is a true shareholder with the same rights, including ownership rights, voting rights, dividend distribution, and economic participation. The blockchain token is not a synthetic instrument, not a price-exposure product, and not a financial product detached from the real world. It is the share itself, expressed as a programmable digital token on a blockchain-based platform.

What changes is how those rights are recorded, transferred, and executed. Tokenized equities enable direct settlement without traditional intermediaries. Transfers occur between allowlisted investors with near-instant settlement — a meaningful improvement over legacy systems that rely on custodians, brokers, and multi-day reconciliation windows. Over time, this onchain representation enables corporate actions such as vesting schedules, governance, and distributions to be executed directly through smart contracts, while still aligning with securities law and maintaining full market integrity.

Rather than replacing traditional finance, regulated tokenized equities bring real-world assets, actual company ownership, into a format that can interact with decentralized platforms, offer fractional ownership, and expand investor access globally. It is the first model in which public and private companies, and crypto-native issuers can express company’s equity on a blockchain without losing the regulatory protections of traditional securities.

Architecture: Centrifuge as Transfer Agent (The Ledger Behind Tokenized Securities)

At the core of this model is Centrifuge’s role as an SEC-registered transfer agent, a regulated institution responsible for maintaining the single source of truth for shareholder records. In a tokenized-equity environment, the transfer agent becomes the anchor that ensures onchain tokenized shares and traditional book-entry shares always match, avoiding the fragmented ledgers often seen in early tokenized assets or wrapped stock tokens. This unified ledger is what allows token holders to directly own underlying shares with the same rights as traditional shareholders.

Centrifuge’s responsibilities include:

- Keeping the official shareholder record across both traditional shares and tokenized shares, ensuring accurate ownership rights and full alignment with securities law.

- Performing KYC/KYB, AML, and sanctions checks on all investors and onchain addresses, similar to the compliance expectations placed on regulated custodians and financial institutions in global markets.

- Operating the smart contracts that represent Caesar’s tokenized equities onchain, ensuring that every token corresponds 1:1 to the real-world equity recorded in the legally authoritative ledger.

- Minting and burning tokens when investors move between traditional formats and tokenized formats, guaranteeing that the digital tokens necessarily reflect the issuer’s corporate records.

- Applying transfer restrictions consistent with the regulatory landscape, including allowlists and investment-eligibility rules, preventing transfers to non-verified wallets across decentralized platforms or centralized exchanges.

- Processing corporate actions: voting rights, dividend distribution, splits, and other events, ensuring that both traditional and tokenized holders receive the same rights and economic exposure backed by the same underlying asset.

Investors interact with this system through two coordinated channels. First, they engage with Centrifuge as a regulated transfer agent: onboarding, registering holdings, and receiving disclosures, much as they would for listed equities or traditional securities. Second, they interact with the onchain layer by holding equity tokens in allowlisted wallets, giving them the benefits of fast settlement, programmability, and the transparency of blockchain technology.

In effect, Centrifuge bridges corporate records, legacy securities infrastructure, and blockchain-based platforms into a single, coherent system, a modern cap table where issuers, investors, and smart contracts all share a synchronized view of who owns the company’s equity. This eliminates intermediaries, reduces operational risks, and gives investors a solid understanding of their real world equities, whether held onchain or offchain.

System Overview: How Tokenized Equities Move Through the Stack

The architecture operates across three tightly integrated layers, each responsible for a different part of how tokenized equities function as regulated financial instruments.

At the top sits the issuer — the company responsible for capitalization, governance, and the corporate formation that defines shareholder rights. This layer determines how ownership rights, voting rights, and obligations will be applied across both traditional shares and their tokenized counterparts. For investors, this is the layer where the economic exposure, dividend distribution policies, and long-term obligations of the company originate, just as they would for publicly-traded companies on traditional stock exchanges.

In the middle sits Centrifuge, acting simultaneously as the SEC-registered transfer agent and the tokenization platform. This is where the official shareholder ledger lives, a legally authoritative digital ledger that records who owns each underlying share, regardless of whether it is held in book-entry form or as a tokenized security.

Here, Centrifuge performs identity checks, sanctions screening, wallet allowlisting, and manages the smart contracts that represent tokenized equities onchain. This is the point where the regulated requirements of the securities industry meet the programmability of blockchain-based platforms.

At the base sits the public blockchain, the settlement layer where the tokenized shares exist when held onchain. The chain provides fast settlement, transparency, and immutable ordering of transfers between allowlisted addresses. Smart contracts enforce who is permitted to receive or hold these tokenized assets, ensuring that every movement respects the issuer’s policies and the broader regulatory landscape. This enables investors to hold fractional shares, transfer equity tokens peer-to-peer, and interact with decentralized platforms, while still staying inside a compliant framework.

Information flows seamlessly downward:

from issuer decisions → into transfer-agent enforcement → into smart-contract execution.

It then flows upward again as onchain events are reconciled back into the legal shareholder register.

The result is a single, synchronized ownership system in which companies, investors, and smart contracts all share the same understanding of who owns the company’s equity. It is how real-world equities become blockchain-based assets without losing the legal clarity or market integrity expected in global markets.

Tokenization and Redemption Flow

An investor begins by onboarding with Centrifuge and adding their approved wallet to the allowlist. Once verified, they acquire underlying shares, recorded in the transfer-agent system just like traditional shares held through a regulated custodian.

When the investor chooses to tokenize, they submit an instruction through Centrifuge’s interface. The transfer-agent system reduces their traditional balance and mints tokenized shares, digital tokens representing the same real-world asset, directly to their allowlisted wallet. These tokens carry the same rights as the traditional equity and are tracked on a blockchain-based digital ledger.

Token holders can keep these shares in self-custody or with custodians connected to the allowlist. Transfers between allowlisted wallets settle onchain and follow the issuer’s transfer rules automatically, attempts to move tokens to unapproved addresses fail, preserving market integrity within the evolving regulatory landscape.

If an investor wants to return to traditional format, they request redemption. The tokens are burned, and their position is restored as book-entry equity. The cap table updates instantly, keeping both representations fully synchronized.

This flow creates a seamless bridge between traditional securities processes and onchain settlement, maintaining investor protections while enabling faster movement and interoperability than centralized systems.

Holding and Transferring Equity Onchain

Once equity is tokenized, it functions much like any other permissioned, asset-backed digital token recorded on a public blockchain, yet it must still operate within the rules that govern traditional shares and the broader securities industry. This creates a system where tokenized equities retain the same rights and protections as traditional stockholders while gaining the fast settlement, transparency, and programmability of blockchain-based platforms.

First, only wallets that have completed onboarding with Centrifuge can hold or receive tokenized shares. This allowlist is enforced directly at the smart-contract level: any attempt to transfer equity tokens to a non-verified address is automatically rejected. This preserves the integrity of the legally authoritative shareholder ledger and ensures that ownership rights and transfer controls align with the existing regulatory landscape, including identity verification and AML requirements.

Second, token holders can choose how they custody their ownership. They can keep their tokenized equity in a self-custodied wallet or work with a regulated custodian that integrates with Centrifuge’s allowlist. In both cases, the beneficial owner recorded in the transfer-agent system—not the wallet—remains the party that legally owns the underlying shares.

Third, transfers between verified participants are essentially peer-to-peer, bypassing traditional intermediaries such as brokers or centralized exchanges. These transfers settle according to the finality rules of the underlying chain and are available 24/7, offering flexibility that traditional stock exchanges cannot match.

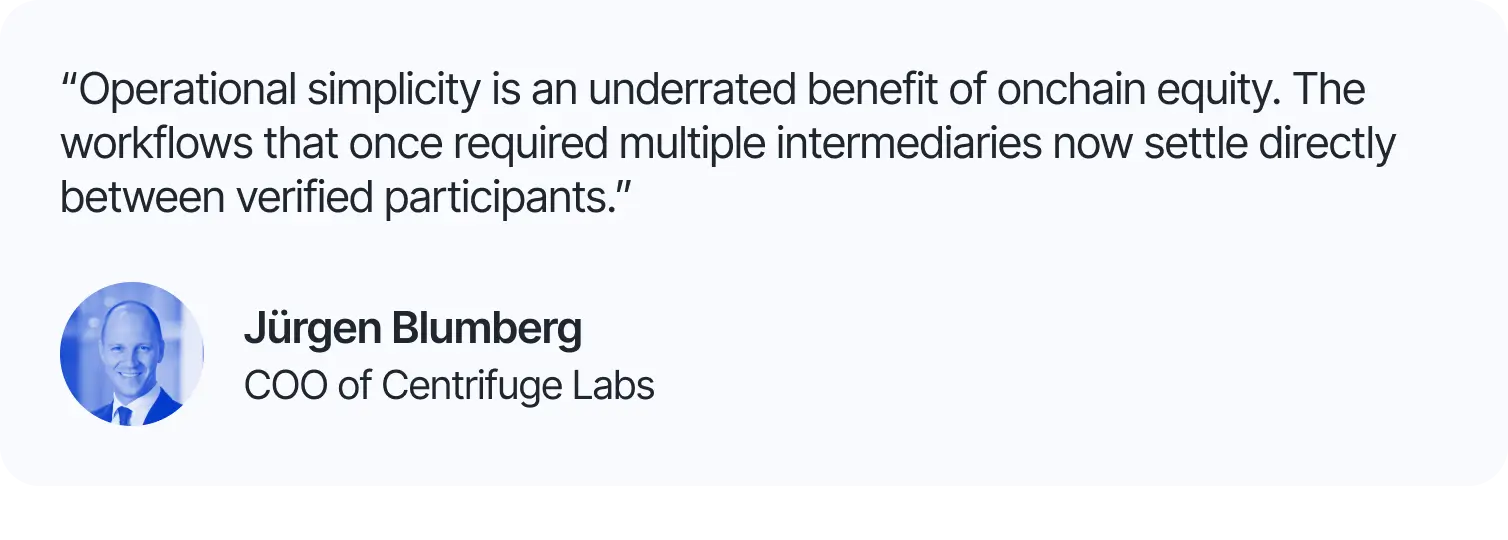

Finally, because Centrifuge logs every mint, burn, and transfer on a shared digital ledger, it can reconcile onchain movements with the offchain shareholder register in real time. This makes corporate actions easier to execute and ensures token holders receive the same treatment as any holder of traditional securities. Corporate workflows that previously required multiple intermediaries are consolidated into a single, synchronized cap-table system.

The outcome is a structure where tokenized equities gain the programmability and instant settlement associated with blockchain technology while remaining fully grounded in the market integrity and legal protections of regulated securities.

The Big Picture for Tokenized Securities

Equity is the next frontier of a broader movement that has already seen fixed-income, fund products, and private credit migrate onchain. Public blockchains offer features legacy systems cannot replicate: shared settlement layers, composability, interoperability, and programmability.

Centrifuge’s model does not discard the existing system. It connects to it. Issuers remain governed by corporate law; Centrifuge remains a registered transfer agent. What changes is the substrate on which ownership is recorded. Tokenized equity represents a reusable, regulated pattern for modern cap table management.

In that sense, this structure is a secure, clean, reusable pattern for regulated onchain cap tables

Sometimes change happens gradually, then all at once. The past decade of tokenization experiments has been gradual; regulated onchain equity, issued directly by the company and anchored in a registered transfer agent, is part of the “all at once” phase.

If this structure proves durable, other issuers can follow a similar pattern: bring equity onchain within the existing regulatory perimeter, using registered transfer agents and clear mapping between tokens and legal rights. Over time, as more issuers and investors adopt this model, liquidity, tooling, and standards can emerge in a way that resembles the rise of ETFs or electronic trading, gradually at first, then more quickly once network effects kick in.

Risks and Open Questions in Onchain Equities

Regulation around tokenized equities and blockchain-based representations of traditional shares is still evolving. Supervisory expectations for onchain securities, broker-dealer activity involving equity tokens, and the status of emerging decentralized platforms or alternative trading venues remain in flux. These regulatory uncertainties shape how quickly tokenized securities can scale within traditional finance and how different jurisdictions classify these digital assets.

Liquidity is not guaranteed. The existence of a tokenized equity does not ensure active secondary markets, tight spreads, or price discovery comparable to publicly traded companies on a traditional stock exchange. Many early tokenized shares may see limited liquidity, trade only via negotiated bilateral transfers, or rely on offchain pricing anchored in private-market valuations. As with any new financial product, adoption depends on market participants, custodians, and regulated institutions being willing to support the asset.

Operational risks remain real. Smart contracts can contain bugs, blockchains can experience outages or degraded performance, and even transfer-agent infrastructure can fail. While careful engineering, audits, and monitoring reduce these potential risks, they cannot eliminate them entirely. The same principles that apply to handling other real-world assets onchain, such as stablecoins or tokenized money-market funds, apply here as well.

Key-management risks also persist. Investors who self-custody tokenized shares face the same challenges as anyone holding digital tokens. If a token holder loses access to their wallet or private keys, Centrifuge can, after verifying identity and reconstructing holdings, burn the lost tokens and reissue them to a new, approved address. This restores ownership of the underlying shares, but it cannot recover unrelated assets held in the same wallet, nor can it remove the inherent responsibilities of managing cryptographic keys.

There is also a broader market-structure question: how quickly will professional trading, arbitrage, regulated custodians, and institutional infrastructure develop around tokenized stocks and regulated onchain equity? The speed of that development will determine how closely tokenized equity prices track traditional valuations, how fractional shares are handled across platforms, and how much volume ultimately migrates to blockchain settlement layers.

These uncertainties do not undermine the model, they simply reflect the seriousness of modernizing the securities industry. Acknowledging the risks is part of responsibly building the next generation of onchain capital markets, where real-world equity can move with crypto-native speed while remaining tied to the same legal foundations that govern traditional finance.

Case Study: Caesar AI and the Evolution of a Crypto-Native Ownership Stack

Caesar AI illustrates how a crypto-native project can evolve from an open, token-driven community into a fully regulated corporate structure, without abandoning its onchain foundations. What began as a decentralized AI co-research collective, where contributors earned utility tokens, coordinated through wallets, and participated in permissionless governance, eventually matured into a company needing enforceable shareholder rights, institutional-grade ownership, and a framework for long-horizon value creation.

To support that evolution, Caesar chose Centrifuge to formalize its corporate structure and introduce tokenized equity as its primary ownership instrument. Rather than migrating into a legacy, offchain system, Caesar elected to represent its equity directly on a public blockchain through Centrifuge’s SEC-registered transfer-agent infrastructure. This model allows Caesar’s shares to exist either as traditional book-entry equity or as tokenized shares with identical voting rights, economic exposure, information rights, and participation in all corporate actions.

Centrifuge’s architecture becomes the operational backbone for this transition: full onboarding and KYC/KYB, the authoritative digital ledger of shareholders, minting and burning of equity tokens, and legally compliant transfer controls. For Caesar, this creates a unified ownership stack where early contributors, new investors, institutional allocators, and future stakeholders can all interact with the same cap table—whether they choose self-custody onchain or traditional custody through regulated institutions.

By adopting real-world tokenized equity, Caesar demonstrates how crypto-native organizations can institutionalize without giving up the openness and transparency of decentralized networks. It stands at the inflection point between hybrid token–equity systems and the emerging category of fully onchain corporate finance—showing how future issuers may modernize ownership, expand their investor base, and scale into regulated markets without severing their onchain DNA.

A Call to Action for Projects Ready to Institutionalize

Many crypto-native projects are reaching the same inflection point. Communities have matured. Contributors expect enforceable, long-term ownership. Institutions and global markets increasingly want exposure to the underlying assets and economic value these organizations create. For teams navigating this transition, tokenized assets, and especially tokenized equity, offer a path that combines the legitimacy of traditional finance with the programmability of decentralized infrastructure.

Centrifuge’s architecture provides the regulated, battle-tested infrastructure required for this next chapter. For projects ready to institutionalize their ownership structure, and to do so while preserving the core advantages of being onchain, Centrifuge is ready to guide that evolution, offering a clear, compliant, and scalable framework for raising capital, managing investors, and issuing equity directly onchain.

.webp)

Ready to get started?

Centrifuge’s real-world asset tokenization platform brings the full power of onchain finance to asset managers and investors.